How can the securities research industry develop with high quality?

The traditional business model of brokerage research institutes is "research for commission", that is, as a seller, providing research services to public funds and receiving their allocated trading commissions.

In 2023, with the reform of public fund rates and the implementation of commission reduction and fee reduction measures, this seller research model has also come to the node of comprehensive research transformation. High-quality research, diversified income generation, all-round collaboration, and digital empowerment have become the new keywords for industry growth.

In many fields, brokerage research is opening up space for value expansion. On the one hand, clients such as private equity, insurance, bank wealth management subsidiaries, industrial capital, listed companies, and local governments have begun to generate diverse and incremental demand for research institutions. On the other hand, the promotion of the registration system and the significant growth in residents’ wealth management needs have promoted brokerages to continuously strengthen their professional capabilities such as asset pricing and product design, provide customers with high-quality services, and further demonstrate the supporting functions of research for their various businesses.

Under the new situation, each brokerage research institute is actively carrying out business model innovation, promoting the two-wheel drive of internal coordination and external services, and transforming to comprehensive research. At the same time, powerful leading brokerages are also investing up the ante digital technology, upgrading the support platform, and empowering the research business, hoping to stay ahead; small and medium-sized brokerages are combining their own resource endowments and seeking opportunities to win from more intense competition through differentiated research. Under the game, powerful analysts and research institutions that build a healthy development mechanism are ushering in the best era.

Source: New Fortune Magazine (ID: xcfplus)

Author: Tang Huijun

Legend has it that at the age of 40, an eagle will fly up a cliff alone, hit a rock with its long and curved beak, causing it to fall off, grow a new beak, and then pluck out the blunt nails and excess feathers one by one, waiting for a new life. After 5 months, the eagle will be reborn and live for another 30 years.

Although the rebirth of the eagle is just a myth, in reality, this phenomenon has been interpreted in many fields. Now, the securities analysts of Eagle Vision have also ushered in this moment.

Under the reform of public fund rates challenging the traditional seller research model, how to improve quality and efficiency, maintain market share, and at the same time expand financial resources and expand comprehensive income; in the historical process of building a financial power, how to cultivate first-class investment banks and investment institutions, and better play the function of capital markets hub, has become a new proposition for the entire securities research and even the securities industry. In the new era, high-quality research, diversified income generation, all-round coordination, and digital empowerment have become the keywords of this industry’s renewed value.

01. Sub-warehouse commissions are shrinking, and revenue is facing challenges

The absolute main force of the securities research industry is the research institutes under the brokerage. Its main income model is "research for commission".

In simple terms, the brokerage research institute will provide research services for institutional investors such as public funds, but the public offering does not pay for this service alone, but is packaged in the stock trading commission paid to the brokerage.

Since the stock trading of public funds is carried out by renting different brokerage seats, the commission received by each brokerage is often allocated by the public offering according to the trading volume in each seat and the quality of the brokerage research services. According to the calculation of CICC, the contribution of investment research services, affiliated funds (brokerages participate in holding funds), channel dropshipping rebates, and third-party service soft commissions to the brokerage sub-warehouse commission income are 40%, 35%, 15%, and 10% respectively, with research services accounting for the highest proportion.

In this model of selling research results in exchange for commissions, brokerage research institutes are also called sellers, while institutions such as public funds are called buyers.

In 2023, the sell-side research model that has been in place for nearly 20 years is being challenged.

The landmark event is that the Securities Supervision Commission announced the "Work Plan for the Reform of Public Fund Industry Rates" in July 2023, and plans to take 15 measures to reasonably reduce fund rates. In December, the Securities Supervision Commission issued the "Regulations on Strengthening the Administration of Securities Trading of Public Offering Securities Investment Funds (exposure draft) " to standardize fund trading commissions and distribution management, and protect the legitimate rights and interests of the Christian people. The reform plan of trading commissions, which is most closely related to the Institute of Brokerages, was clarified, and the reduction of commissions became a foregone conclusion.

According to the new regulations, passive funds such as index funds are not allowed to pay for research services through trading commissions, and their commission rates will be linked to the market average; the commission rates for other funds to pay for research services shall not exceed twice the market average in principle. At the same time, when a fund manager trades through a brokerage, the commission allocated to the brokerage shall not exceed 15% of the total commission of the fund for the year. For small equity funds with a management scale of less than 1 billion yuan, the distribution limit of 30% can still be maintained.

So, what is the impact of this public offering cut on brokerages?

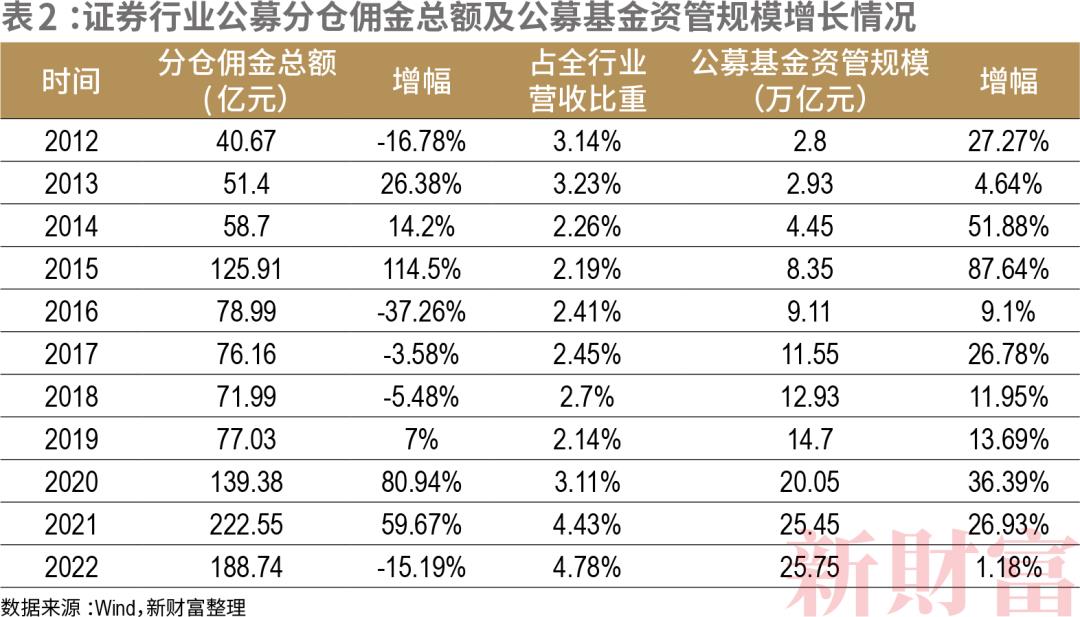

Its core comes from the impact of the reduction in the commission rate of the sub-warehouse. If the ratio of the sub-warehouse commission to the total turnover of public fund stocks is used to roughly estimate the sub-warehouse commission rate, it can be found that from 2018 to 2022, the sub-warehouse commission rate decreased from 0.084% to 0.076%. According to the calculation of Huachuang Securities Research Institute, the average commission rate of the class A share market decreased from 0.035% to 0.025% in the same period (Table 1).

Brokers’ commission rates for sub-positions are much higher than the market average, which should be related to their value-added services such as seller research. According to the new regulations, if the commission rate for sub-positions drops to twice the market average, it will be 0.04% to 0.05%.

According to CITIC Securities Research Report, considering only the adjustment of commission rates, it is expected that the size of the class A share market seat rental commission may drop from 18.87 billion yuan in 2022 to 12.64 billion yuan, a decrease of 33%.

Looking at it for a long time, although public funds have ushered in a period of rapid development in recent years, the size of their assets under management has increased from 2.80 trillion yuan in 2012 to 25.75 trillion yuan in 2022, an increase of more than 8 times, while the sub-warehouse commissions obtained by the securities research industry during the same period have only increased from 4.067 billion yuan to 18.874 billion yuan, an increase of 3.6 times (Table 2). The lagging growth rate of sub-warehouse commissions means that even if the scale of public offerings continues to expand in the future, the sub-warehouse commissions may not increase simultaneously.

In addition, the level of sub-warehouse commissions is easily affected by market conditions: with the arrival of a bull market, the scale of public fund management has surged, and transactions are active, commissions often jump; if the market lingers and transactions are light, commissions will also be affected, and the amount in 2022 will decline significantly compared with 2021.

While income growth is not high or stable, the securities research industry has continued to expand in recent years.

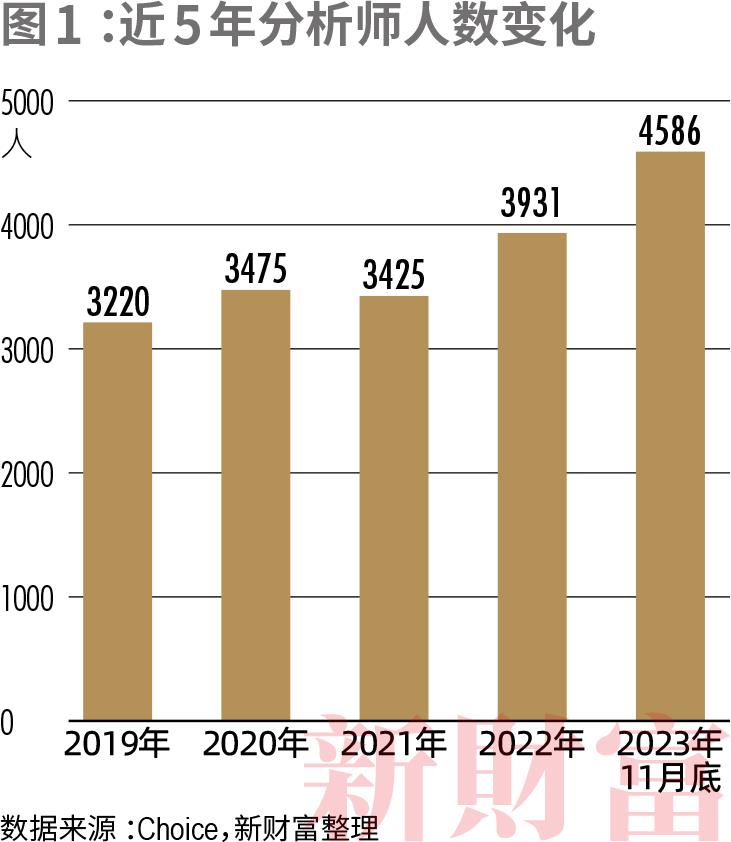

Choice data shows that as of the end of November 2023, the number of analysts registered with the Securities Industry Association has reached 4,586 (Figure 1), and the number of brokerage institutes with more than 100 people has also increased from 6 in 2019 to 13 in 2023.

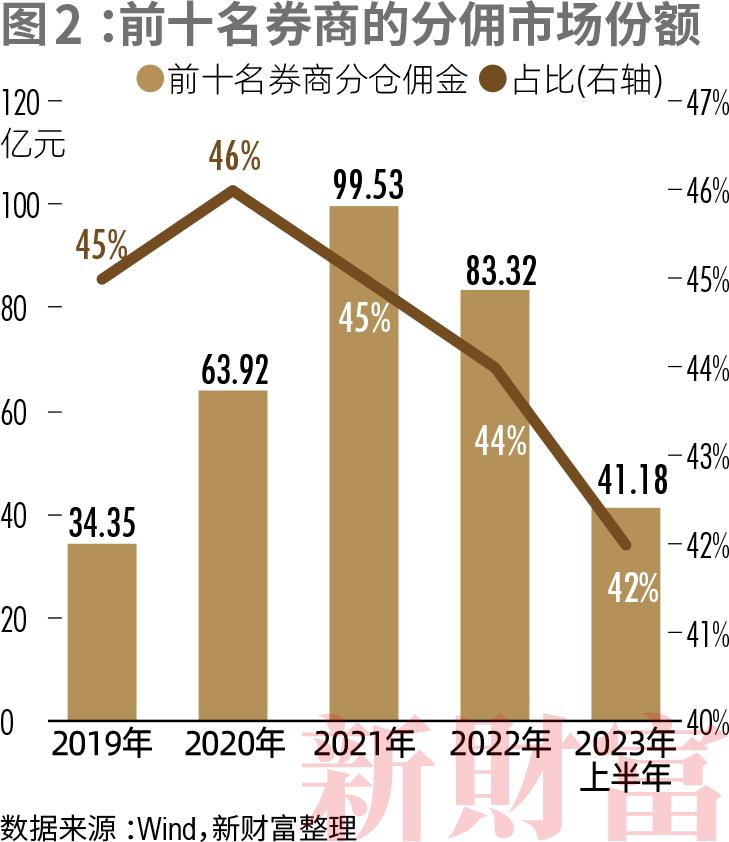

The increase in the number of employees has intensified the competition in the securities research industry. Data from the past five years show that the share of sub-warehouse commissions of the top ten securities firms has continued to decline, from 45% in 2019 to 42% in the first half of 2023, and the industry concentration has declined (Figure 2).

Looking to the future, the asset management scale of public funds is still growing. A milestone event is that by the end of June 2023, the total net asset value of public funds in the country reached 27.69 trillion yuan, exceeding the scale of bank wealth management products of 25.34 trillion yuan for the first time. Public funds also replaced bank wealth management and became the "asset management brother".

Data from the China Securities Investment Fund Industry Association shows that as of the end of the third quarter of 2023, the total scale of asset management business of public fund management companies and their subsidiaries, securities companies, futures companies, and Private Offering Fund management institutions is about 67.60 trillion yuan, of which 11,221 public fund products The total scale reached 27.48 trillion yuan; and at the end of 2022, the total scale of public fund management was 25.75 trillion yuan.

In recent years, the scale of bank wealth management products has been shrinking, among which the proportion of fixed income products has increased, and the scale and share of public fixed income funds have also shown a double increase trend, reflecting the increasing urgency of residents’ willingness to preserve and increase the value of assets. With the advancement of rate reform, the enhancement of innovation such as floating rate products, and the expansion and expansion of public offering REITs, public funds are expected to maintain a top position in the competition in the wealth management market.

But under the high proportion of fee reduction, it is still unknown whether the commission cake will expand, and the competition in the securities research industry will undoubtedly become more intense in the future. How to break the high dependence on public offering sub-warehouse commissions and seek diversified income paths has become an urgent new challenge for securities research institutes.

02. Diversified income generation, a great era of value expansion

In fact, from seller research to comprehensive research, serving a wider range of customers, and achieving diversified income generation, the securities research industry has been solving problems for a long time, and many research institutes have made useful explorations. This reduction in public fund rates is just another node to accelerate the transformation.

In accepting the new wealth survey, many directors of securities research institutes pointed out that with the continuous development of capital markets, the research business is ushering in a great era of value expansion, and its customers have not only expanded to insurance companies, social security funds, private equity and other institutional investors. In recent years, demand from bank wealth management subsidiaries, industrial capital, listed companies, local governments, etc., has also brought broad value realization soil and development space for securities research.

Asset management business brings added value

The development of China’s economy and the establishment of a well-off society have led to the rapid growth of the wealth management market. In the wealth management market, public funds, which are the main service targets of analysts, account for only about 20% of the assets under management (Figure 3). Other institutions are also generating new demand for research, including bank wealth management subsidiaries similar in size to public offerings, and qualified foreign institutional investors (QFII) who are heating up.

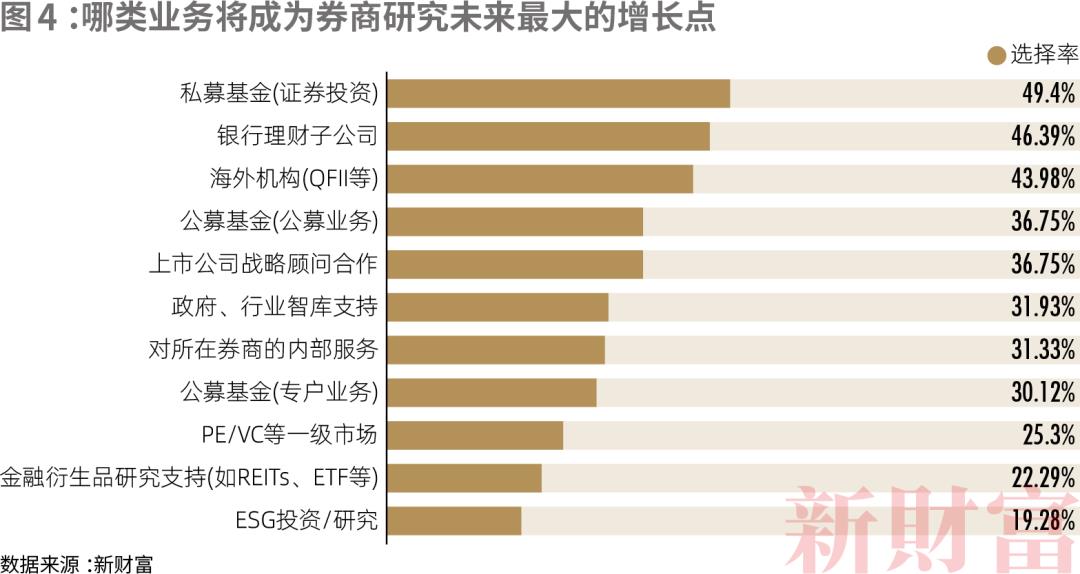

New Fortune’s 2023 survey shows that in the face of market changes, more than 40% of analysts believe that demand from Private Offering Funds (securities investment), bank wealth management units, QFII, etc. will become the largest growth point for brokerage research in the future (Figure 4).

Although the scale of private securities investment funds is relatively limited compared to public funds, in recent years, the proportion of private securities investment funds has been increasing (Table 3). At the same time, the number of private equity managers with a scale of over 10 billion is also on the rise. According to the data of private placement network, as of December 19, 2023, the number of private securities managers with 10 billion private securities reached 104, while in 2020 there were only 52. With the growth of leading private equity managers and the obvious differentiation of fund performance, private equity managers with mature investment concepts, excellent long-term performance and strong risk control capabilities will be more favored by the market in the future, which also means that their demand for professional research will be stronger.

Not only that, the continuous expansion of primary market investment scale such as Private Equity funds and venture capital funds has also driven the rapid development of the Private Offering Fund industry. According to the data of the Securities Investment Fund Association of China, in mid-2022, the asset management scale of China’s Private Offering Fund industry officially crossed the 20 trillion mark. Among them, Private Equity funds and venture capital funds accounted for 53.87% and 13.21% respectively. Private equity funds usually invest in unlisted or long-maturity enterprises with a longer holding period. Its characteristics determine that private equity investment requires a highly specialized investment team and research capabilities. In this process, research support is indispensable.

In addition to Private Offering Funds, bank wealth management subsidiaries are also expected.

In 2022, the new asset management regulations will be fully implemented, and the transformation of the net worth of wealth management products will continue to deepen. In the context of rigid redemption being broken, how to launch stable high-yield products, especially stock-based equity products, has become a pain point for bank wealth management subsidiaries.

For example, the first equity product launched by Everbright Wealth Management, the Sunshine Red Hygiene and Safety Theme Selection, saw its net value fall by more than 20% in 2023. Extending the timeline, this product established on May 26, 2020, saw its net value fall below 1 yuan on August 17, 2021, and has now fallen below 0.5 yuan, with the yield worsening.

And this is not an isolated case. The reason is not difficult to understand. Banks that are good at credit and bond business have always had a weak investment and research system for equity assets represented by stocks. Therefore, the wealth management subsidiaries that were born out of banks are not good at the operation of equity products.

In the past, the asset management departments of most banks did not form a complete equity investment research system due to low risk appetite, inability to directly invest in stocks, and low degree of marketization. After the opening of the wealth management subsidiary, the restrictions on its investment in stocks were liberalized, and it became the general trend to increase the allocation of equity assets in the future. Some institutions predict that in 2030, the scale of stock investment brought by China’s wealth management products is expected to reach 5.50 trillion yuan.

The banking financial registration and custody center released the "China banking financial market semi-annual report (2023) " shows that as of the first half of 2023, the approved opening of bank financial subsidiaries has reached 30, financial products asset allocation to fixed income-based, the proportion of equity-based assets is only 3.25%, equity-based assets balance of 900 billion yuan, equity-based products only 80 billion yuan, there is still a very broad space for growth.

On the other hand, State Street Global, a leading bank asset management company, invested 61.5% of its equity assets at the end of 2018, and State Street is also the largest bank asset management company in the world by asset management scale (AUM).

With the gradual entry of huge wealth management funds into the market, bank wealth management may become an important incremental market for securities research. The equity research system of securities research institutions is mature and the industry coverage is complete, which can better adapt to the needs of wealth management subsidiaries.

Everbright Securities Financial Industry Chief Analyst Wang Yifeng once said that after years of development, securities firms have accumulated strong investment research strength and investment experience, and strengthen inter-industry cooperation with bank wealth management subsidiaries, which can enhance the active level of equity investment in the latter, so that it can quickly make up for the shortcomings.

A person in charge of a securities firm said that the seller research institution can provide special project investment and research support for the credit bond investment, pan-market value management and asset allocation of the bank’s wealth management subsidiaries, and can strive for relevant asset management and brokerage business opportunities. At the same time, securities firms can strengthen cooperation with wealth management subsidiaries in product design to help them achieve stable returns.

In fact, there are already many brokerage research institutes actively seeking cooperation with bank wealth management subsidiaries. More than 10 brokerage research institutes in the new wealth survey found that although there is no stable value exchange model between the research institutes and bank wealth management subsidiaries, they have been regarded as important potential customers, and some research institutes have established professional teams to serve them.

Ding Wentao, the current executive committee member, assistant president and chief strategy officer of Soochow Securities, said in a new wealth survey in 2023 that the service bank is a very important end of the Soochow Securities Research Institute. "We should have established a bank sales team earlier in the industry. At present, the service bank team is nearly 10 people."

In the Class A share market, QFII is also a force to be reckoned with.

In July 2003, UBS completed the first foreign purchase of class A shares through QFII. In 2023, QFII ushered in the 20th year of investing in class A shares. According to the data released by the Securities Supervision Commission, as of November 2023, there were 802 qualified foreign investors in the whole market, including QFII and RMB Qualified Foreign Investors (RQFII) institutions. Among them, there were 10 QFII institutions with a quota of more than 2 billion US dollars, including the Abu Dhabi Investment Authority, the Macao Monetary Authority, the Bank of Korea, Socie ? te ? Ge ? ne ? rale, Barclays, and the Norwegian Central Bank.

According to Wind data statistics, as of November 1, 2023, 48 QFII companies have appeared in the list of the top ten circulating shareholders of 804 class A share companies, and the total market value of QFII positions has reached 141.831 billion yuan. Heavy warehousing industries include pharmaceutical biology, electronics, non-ferrous metals, building materials, power equipment, etc., and the market value of positions exceeds 5 billion yuan.

In response to foreign investment, many research institutes have already formed teams to provide services, and there is still room for deepening services in this market in the future.

Listed company strategy consulting

Not only the asset management industry, with the opening of the Science and Technology Innovation Board and the Beijing Stock Exchange, the multi-level capital markets continue to mature, the rapid expansion of listed companies has also begun to generate new demand for research.

Search for outstanding listed and proposed listed companies, provide them with strategic advice, help them grow and develop, and serve as a bridge between enterprises and investors, becoming one of the sources of incremental value for the securities research business in the new era.

The core job of an analyst is to mine and interpret various types of information related to listed companies, providing reference for institutional investors in the secondary market. As the research continues to deepen, their understanding of the industrial chain covered will also become increasingly profound. In the current era of rapid iteration of business models and industrial logic, analysts with deep knowledge in industrial chain research can provide companies with forward-looking opinions, help them clarify the competitive situation, understand industry trends, and combine their own endowments to extend the value chain. Analysts can also use rich resources such as industry experts to build a communication and docking platform for listed companies.

At present, corporate clients have become a key service group for many comprehensive brokerage research institutes. Zhou Haichen, general manager of Shenwan Hongyuan Group Research Institute, told New Fortune that providing enterprises with industrial chain research, such as industrial services, expert services, and industry research, is a very important end of their business.

"It’s a bit like McKinsey. For example, if some companies want to invest in new energy, they may need us to help them sort out the entire new energy industry chain, do some value evaluation reports, strategic planning, etc. Because there are many listed companies now, the market potential of this area is relatively huge."

At present, there are more than 5,000 listed companies of class A share, and most of them have entered the field of vision of different research institutions, that is, analysts have some understanding of them. According to Choice data, from January to November 2023, 87 securities companies released nearly 170,000 research reports, covering more than 60% of listed companies of class A share.

Generally speaking, the research institute has always tended to cover listed companies with high market capitalization and investment value. Taking CICC as an example, Choice data shows that from January to November 2023, the total number of companies covered by its research report exceeded 1,000, accounting for about 1/5 of the number of listed companies in class A shares, and the market value accounted for nearly 60%. However, although few analysts are interested in companies with low market capitalization, they will also have consulting needs. Analysts who have been deeply involved in the industry for a long time may be able to help them grow.

It is worth mentioning that the increasingly hot ESG research has also become an important means for securities research institutions to promote the high-quality development of listed companies. By actively communicating with listed companies, securities research institutions can assist them in improving ESG ratings, uncovering the sustainable development value of enterprises, and making them reflected in market value, thus forming a virtuous circle.

Join hands with the government to act as a "think tank" to help regional economic development

The value increment of another part of securities research comes from local governments.

As China’s economy enters a period of transformation and industries enter a period of upgrading, the demand for policy advice from policymakers at all levels is growing day by day. For local governments, it is their important mission to identify industries that represent the future direction, attract leading enterprises in the process of attracting investment, and promote the growth of local strategic emerging industries to achieve high-quality economic development.

Analysts can provide advice to local governments based on their in-depth understanding and research of industrial development trends and the competitive advantages of different companies, helping them adapt to the general trend of the industry, guiding promising enterprises to land, guiding funds to focus on local high-quality companies, and achieving a positive interaction between capital and industry.

Especially for securities firms with local state-owned assets background, based on regional economic development, we provide think tank support for policy formulation and industrial development for government departments, industry associations and other organizations, and build a communication platform to enhance the exchange between capital and local government and industry. This has become another direction for securities research institutes to export research value and achieve differentiated transformation.

At present, more and more brokerage research departments work closely with local governments, and have carried out organizational restructuring to empower local governments based on the national strategy of financial services and the real economy.

Wang Bin, assistant to the president of Industrial Securities and dean of the research institute, told New Wealth that the Industrial Securities Research Institute has set up a think tank research center and established a think tank research team. By integrating research resources, it serves external local governments and regulatory departments, and provides internal strategic research services to help the development of the company’s various businesses. At present, Xingzheng Think Tank is the first batch of 15 key think tank construction pilot units in Fujian Province, and has been selected as the first batch of eight Shanghai CPPCC consultation think tank units.

Some regional brokerage research institutes give full play to their location advantages, highlighting their characteristics and regionalization. Ding Wentao said that Soochow Securities is headquartered in Suzhou, and the important goal of the research institute is to establish a foothold in Suzhou, serve regional development and local listed companies, and form effective synergies with the local economy.

Suzhou is one of the most active regions in the domestic economy, with considerable real economic resources. At the beginning of 2023, the number of class A share listed companies in Suzhou has exceeded 200, ranking fifth in the country. These companies focus on the four major industries of electronic information, equipment manufacturing, biomedicine, and advanced materials. In order to echo the local real industry, Soochow Research has also focused on attacking and strengthened the allocation of relevant research teams.

Ding Wentao said that in terms of research layout, Soochow Securities Research Institute does not blindly pursue industry-wide coverage, but prioritizes effective resources to the core areas and firmly grasps the advantageous industries. For these four advantageous industrial clusters, Soochow Securities Research Institute organizes at least four special conferences every year, and widely invites local listed company representatives, industry experts, local government representatives and institutional investors to participate, so that the market can fully understand Suzhou enterprises and help local industries "go global".

The Zheshang Securities Research Institute, which is also a regional brokerage, has the slogan of "deeply cultivating Zhejiang, embracing banks, and deepening the industry". Qiu Guanhua, chief strategy officer of Zheshang Securities and director of the research institute, said that "Zhejiang is fertile ground for high-quality listed companies. Zheshang should be the research institute that has the broadest and deepest research on listed companies in Zhejiang Province, the best tracking, and the most complete and best service. Let investors in the market think of listed companies in Zhejiang, and they will naturally find the Zheshang Securities Research Institute."

Deeply involved in the Guangdong-Hong Kong-Macao Greater Bay Area, Yuekai Securities, a subsidiary of Yuekai Research Institute, is committed to "building a first-class think tank that is the pearl of the Greater Bay Area", with government departments, institutional customers, and Bay Area enterprises as the main service objects. In 2023, the report "Guangdong-Hong Kong-Macao Greater Bay Area: New Pattern and Grand Strategy" will be launched, providing suggestions for the high-quality development of the Greater Bay Area from four key areas such as industry, technology, finance, and public services.

03. All-round collaboration to explore internal support paths

While exploring ways to realize diversified value, the Institute also began to seek to provide more intellectual support in the internal changes of securities firms.

In the construction of modern capital markets with Chinese characteristics, the reform of the securities industry is also deepening. Building a "three-investment linkage" mechanism for investment research, investment and investment banks, and improving the professional service ability of "customer-centered" have become the core of the competitiveness of securities firms.

Especially under the full implementation of the registration system, investment banking business began to be deeply bound to research. Under the registration system, the issuance of new shares adopts market-oriented pricing and underwriting mechanisms, and the number of new shares is no longer scarce, and listing breaks have become a common phenomenon. How to price reasonably tests the skills of investment banks. In addition, in the new round of technological change, there are more and more listed companies in new models and new industries. In their IPOs, mergers and acquisitions, and fixed increase businesses, the understanding of enterprises cannot only stay at the financial level, but also based on the professional perspective of the industry, to issue persuasive opinions. Analysts, with their understanding of the industry, have a say in evaluating the long-term investment value of companies and enhancing the rationality of pricing. Their research results can become an important reference for investment banks to develop their industries.

At the same time, as brokerages have established alternative investment subsidiaries and private investment subsidiaries to extend their business to IPO follow-up investment and Private Equity, the coordination of research departments has become more important when they explore high-quality targets.

Many professional investment banks and investment teams have been deeply involved in sub-sectors for many years, and their research understanding of industries and enterprises is also in place, which can form a benign interaction with the research institute and promote the overall improvement of the general capabilities of securities firms.

Lu Ying, then director of Haitong Securities Research Institute, told New Wealth: "Many technology startups are willing to communicate with professional researchers. The investment banking department has also complied with the requirements of the real economy and Enterprise Services, dividing industry groups, such as special technology teams, medical teams, etc. These teams are naturally more cohesive with research in terms of professionalism."

"Our cooperation with investment banks is not only in IPOs or fixed growth, but also in industrial research on the enterprise side to expand the comprehensive service capabilities of Guojin Securities," Su Chen, director of the Institute of Securities Research, said in an interview with New Wealth.

Another person in charge of the investment banking department of a brokerage said: "From the perspective of cooperation, investment banks, research institutes and alternative subsidiaries determine whether a company meets the positioning and audit requirements of the Science and Technology Innovation Board after professional research; from the perspective of division of labor, investment banks, research institutes and alternative subsidiaries independently judge whether a company meets the relevant conditions from their own perspectives. Under the conditions of this cooperation and division of labor, the enterprises selected by the sponsor institutions are truly in line with the national strategy, market requirements and positioning of the Science and Technology Innovation Board." This also confirms that the coordination between the research institute and other institutions within the brokerage firm has become increasingly important.

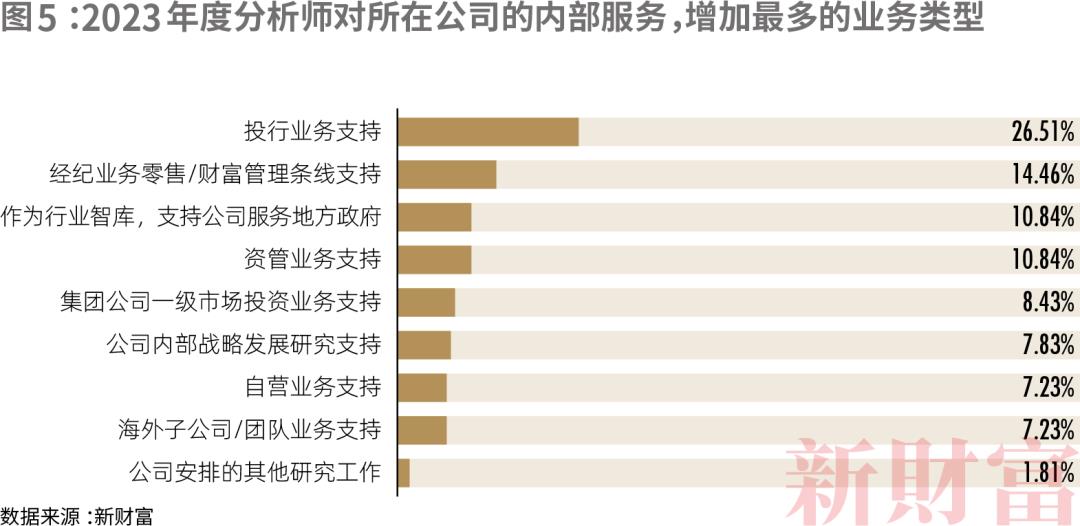

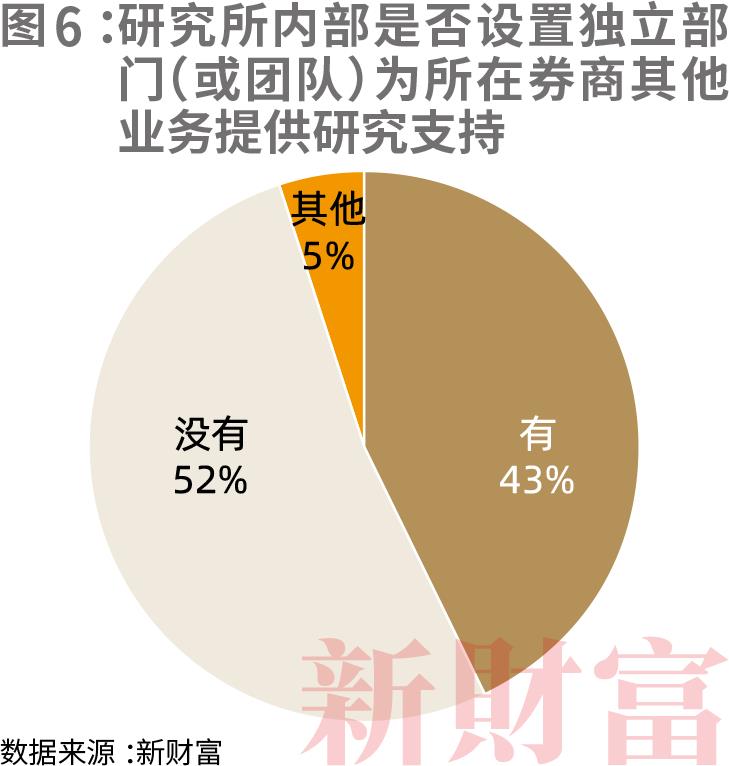

New Fortune’s 2023 survey of analysts shows that support for investment banking, proprietary, asset management, and brokerage services has become an important source of incremental demand in their internal services (Figure 5). Currently, 43.37% of research institutes have set up independent departments or teams to provide research support for other businesses within their brokerages (Figure 6).

In the internal support work, research support for investment banks is the mainstream, followed by support for brokerage/wealth management lines.

In the past, brokerage was the basic business of securities companies and was at the front end of marketing. Its core was the ability to acquire customers under the license, and its income mainly came from the commissions paid by customers for securities transactions. Today, the channel-type brokerage business is in the process of transforming into a wealth management business. The core of the wealth management business is "customer-centric". Brokers must create value for customers and realize the preservation and appreciation of their assets in order to obtain profits. Under this model, the research and allocation of large types of assets is increasingly important. How to develop more popular products in the market becomes the core, and this also requires the empowerment of the research department.

At the same time, the expansion of wealth management business requires a professional team of investment consultants to help clients allocate assets according to their own needs. Brokerage research institutes can also endow their own research capabilities to investors to deepen their understanding of the intrinsic value of products, macro directions, and investment strategies, so as to better serve customers.

In 2021, at the suggestion of Huang Yanming, director of Guotai Junan Securities Research Institute, Guotai Junan Securities launched the "Investment Advisory Jincai" plan, a joint research institute of the Wealth Management Commission, to classify investment advisors and submerge research resources into branches to help investment advisors improve their investment concepts, enhance their professional capabilities, and create more opportunities for their career development.

In Huang Yanming’s opinion, the service system of brokers to institutional investors has become more perfect. In contrast, although the financial products of brokers to serve small and medium investors are constantly abundant, there are many shortcomings in the professional ability of the investment advisory team as a whole, which is not enough to support the growing wealth management needs of residents. "At present, the majority of residents are more in need of professional investment consulting services to solve problems such as’funds make money, Christian people lose money ‘and’chasing up and selling down’." As the department with the most resources and the strongest research ability of brokers, the research institute has a lot of room to do in this regard.

China Merchants Securities Research Institute has also practiced the operation mode of internal services earlier. It has a research department and a research department. One is dedicated to external services, mainly for customers such as public funds and insurance institutions. The second is dedicated to internal services, mainly for brokerage and other businesses. A clear trend is that whether or not a full-time external or internal service department is established, the comprehensive nature of research business is becoming prominent.

And those large securities companies, with the accumulation of comprehensive service experience, the effect of empowering each other between platform and research is becoming increasingly prominent. On the one hand, strong research strength and good reputation can help them form a strong customer acquisition ability and enhance their comprehensive strength; on the other hand, the enhancement of comprehensive strength will further feed back the research business and form a joint force to help securities firms gain an advantage in the fierce market competition.

In this process, the positioning of the research business often follows the company’s Strategy and Development Goals. Platform development requires research to form a strong cooperation with various business departments within the brokerage, further empowering investment banking, asset management, self-management, brokerage and other businesses, and enhancing the comprehensive service capabilities of the brokerage.

For example, the National Securities Research Institute launched the research 3.0 reform in 2020, establishing a strategic goal of "investment banking as the traction and research as the driving", while the research institute was redefined as a non-profit department. "The 3.0 reform of the research institute aims to generate revenue, reputation and market influence. This change will actually drive the branding impression of the company as a whole and the development of other business sectors, which is also an original intention of our transformation," Su Chen told New Fortune.

In fact, this process (research business integration transformation) is quite similar to the evolution of the overseas securities research industry.

In 1975, the United States abolished the 185-year-old fixed commission system. After that, the commission rate fell from 0.5% in 1975 to 0.06% in 2001. At the same time, the introduction of the storage shelf issuance system (one approval, multiple issuance refinancing system) in 1983 increased the flexibility of financing. These reforms intensified the competition of investment banks in traditional fields, and the big investment banks began to seek transformation and evolve into all-round investment banks.

In this context, Goldman Sachs restructured its business model and quickly became a world-class investment bank. In terms of business model, Goldman Sachs is positioned as an all-round investment bank. Investment banking, mergers and acquisitions, market making, derivatives and other business lines are built around the needs of institutional clients. It provides comprehensive and professional services. Its ultra-high risk pricing capabilities have become the core support for investment banking to develop its business. And pricing capabilities are the core value of research business.

Goldman Sachs’ institutional business segments mainly include equity and FICC (Fixed Income, Currencies and Commodities, Fixed Income, Foreign Exchange and Commodities), among which, equity business includes brokerage, margin financing, stock and derivatives market making, PB, etc.; FICC business includes interest rate, exchange rate, credit, commodity market making and trading.

In the continuous evolution of the market, the needs of institutional clients have also become more diverse. After entering the 1980s, asset management became one of the core business of investment banks, because as the proportion of assets managed by overseas institutional investors continued to increase, their needs for investment banks also became more diverse. In addition to brokerage, underwriting and other businesses, there are more needs for comprehensive wealth management, mergers and acquisitions integration. The diverse needs in turn have also promoted the continuous development of research business, and the comprehensive transformation of research business has become the general trend.

Nowadays, the "institutionalization" of China’s capital markets is also constantly evolving. Especially in the context of the comprehensive registration system, the listing conditions are more diverse and the listing efficiency is significantly improved, which will provide more high-quality assets for long-term funds and further enhance the attractiveness of the market to institutional investors. From an investment perspective, institutional investors often look for pricing deviations in the market based on fundamentals, discover undervalued stocks, and obtain excess returns. Therefore, the research business with asset pricing power as the core is increasingly valued by institutions.

Change is happening. Judging from the more than 10 research institutes in the New Wealth Survey, the vast majority of them emphasize comprehensive positioning.

Wang Bin said that the Industrial Securities Research Institute has added an industrial research center and a think tank research center, among which the industrial research center is committed to fully empowering the company’s investment banking business and forming a product R & D linkage business model; the think tank research center is designed to serve external government and regulatory departments as well as internal strategic research.

Xu Xingjun, general manager of GF Securities Development Research Center and chief analyst of the electronics industry, also said that the research institute will continue to integrate into the company’s institutional customer comprehensive service chain on the "one GF" stage, coordinate various business lines, and provide customers with a package of services including research, trading, market making, derivatives, etc.

In the past, due to problems such as the difficulty of quantifying internal services, analysts lacked enthusiasm for internal services. Now, the internal service mechanism has begun to mature, and many research institutes have gradually formed a relatively stable value exchange mechanism.

Shao Linlin, director of the SDIC Securities Research Institute (formerly known as Anxin Securities), told New Wealth: "At present, the research institute adheres to the principle of one SDIC, which is based on meeting customer needs in an all-round way. Business coordination is achieved through the internal research service platform. When departments have demand for research, they can submit the process on this platform. During the process, the service form and settlement method will be clarified."

Shenwan Hongyuan Group Securities Research Institute has also formed a relatively stable internal value exchange mechanism. Zhou Haichen introduced that in the process of serving investment banks, the institute adopts a flexible fee model of "fixed + floating". By setting scoring weights, the fixed fee part is determined, which can not only pay for the researcher’s "hard work", but also encourage the researcher’s willingness to serve; and finally, according to the researcher’s workload and performance, additional points are given to the researcher, which constitutes the researcher’s flexible income.

Although currently serving institutional clients primarily funded by public funds remains the main source of income for brokerage research institutes, the proportion of internal synergies is gradually increasing.

04. Go deep into the industry and do high-quality research

Whether it is strengthening internal coordination or expanding external customer types, the essence of research has never changed behind the changing business model. Its origin remains "research creates value".

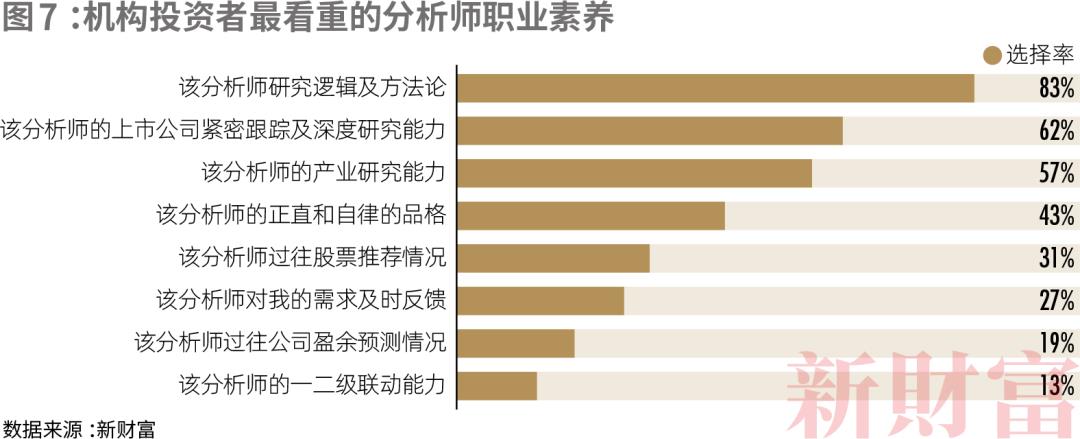

Valuable research must be high-quality research. Quality is still the key to impressing buy-side institutions. New Wealth found in the survey that buy-side institutions have a very strong demand for in-depth reports and are willing to pay a higher premium for in-depth and high-quality research in the long run. Analysts’ research logic and research methods, close tracking of listed companies and in-depth research capabilities have become the most valued professional qualities of buy-side institutions today (Figure 7).

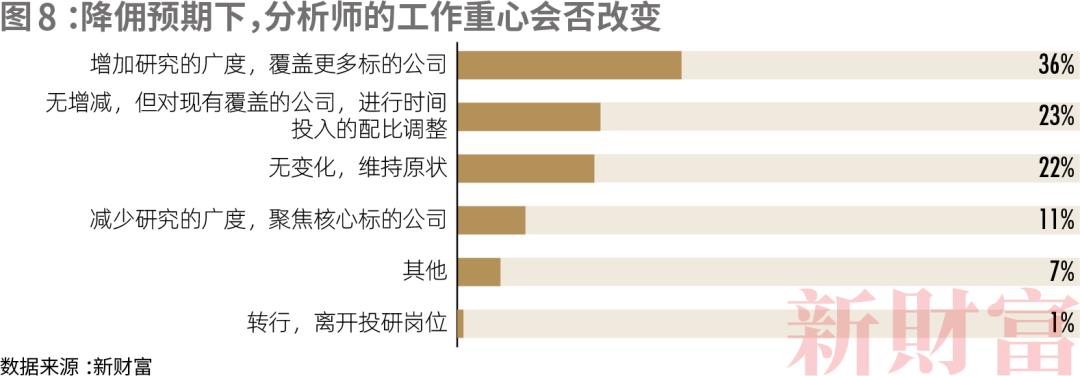

On the road to high-quality research, analysts have also adopted different coping strategies (Figure 8).

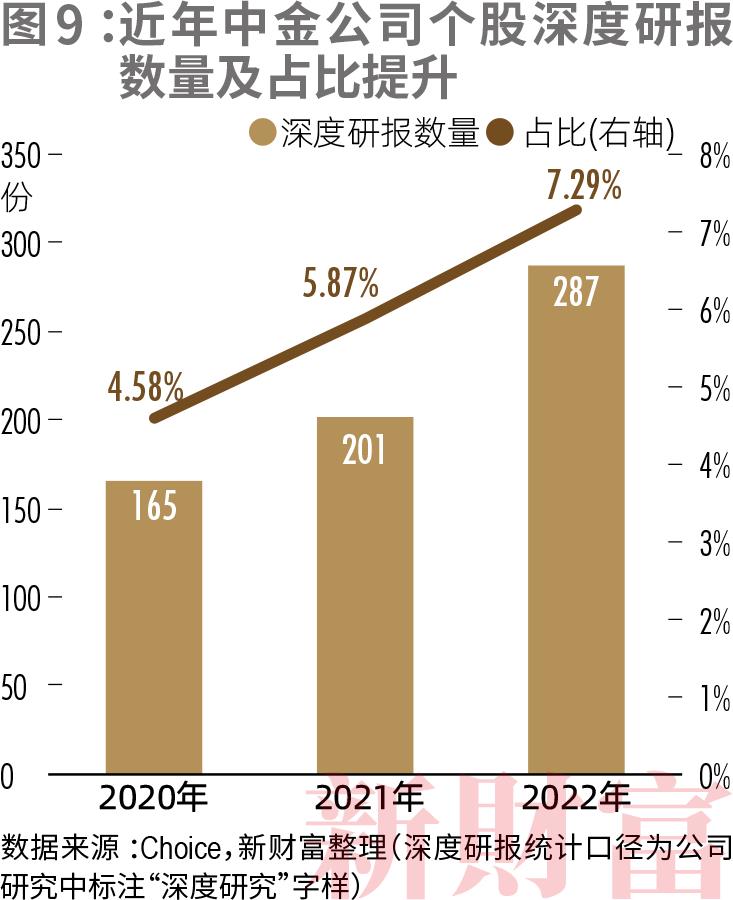

Behind the call for the return of research business to its roots is the market’s expectation for in-depth research. Many brokerages have begun to adjust in this direction. Take CICC’s stock research as an example. In the past three years, the number and proportion of in-depth research reports in its corporate research have increased significantly (Figure 9).

In Su Chen’s opinion, the so-called in-depth research can be judged from several aspects: "The first criterion is whether the research is forward-looking, for example, whether the research can bring effective inspiration to investors; the second is whether the research has withstood the test of the market, which can even be said to be the only criterion for judging whether the research is deep, forward-looking, and whether it is recognized by the buyer; the third is the series of research. In-depth research cannot be like’bear breaking rice ‘. Studying this today and studying another hot spot tomorrow is also an important criterion for the sustainability of industry research."

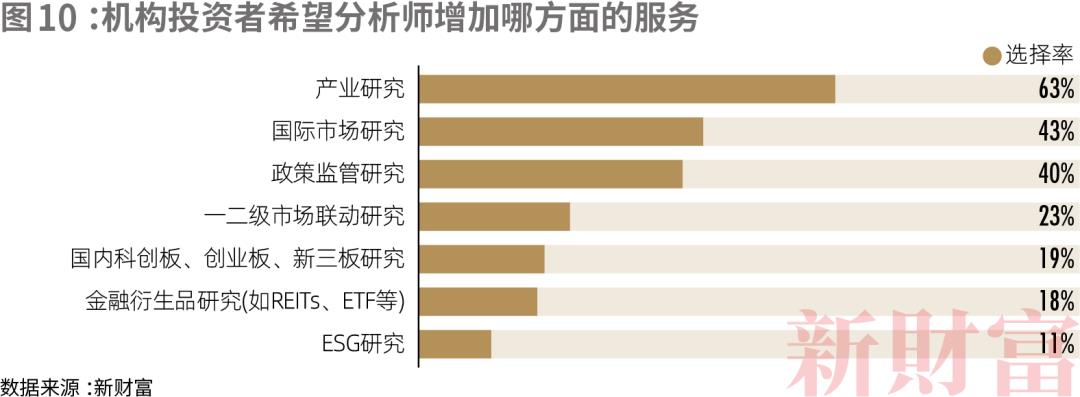

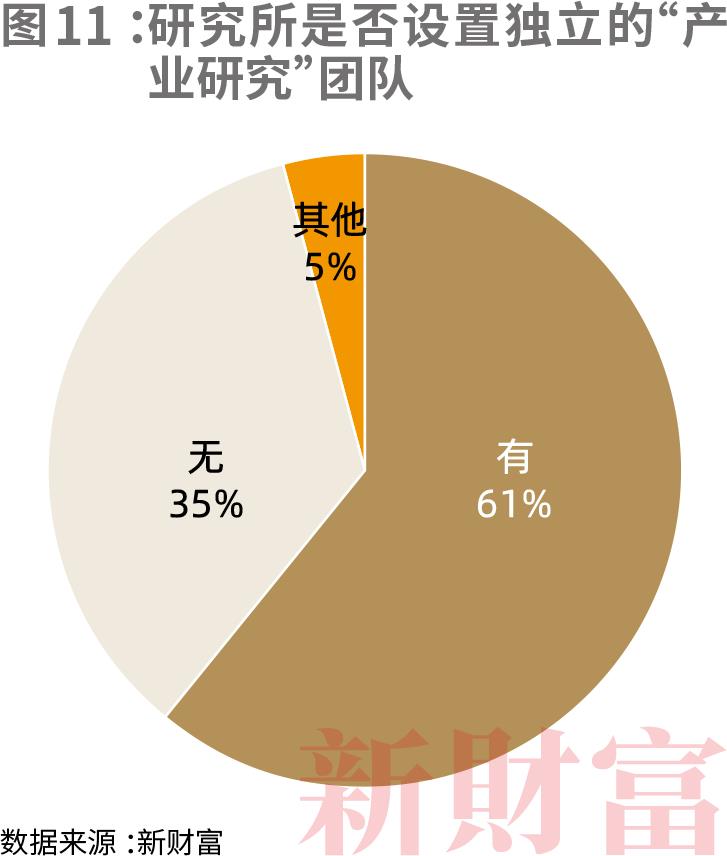

Under the in-depth research, industrial research has become the mainstream demand of institutional investors (Figure 10). More than 60% of the surveyed securities research institutes have set up independent "industrial research" teams to provide intellectual support to listed companies, local governments and other customers (Figure 11). This requires not only analysts to have a long-term perspective, but also a deep industrial chain perspective.

In fact, in order to meet the needs of investors, the scope of securities research has also covered macroeconomics, medium-sized industries to micro-listed companies, and the research objects have also expanded from stocks, bonds, derivatives to commodities, fund portfolios, etc. The research span extends from industrial trends and market trading strategies to medium and long-term trends and judgments.

As a bridge linking industry and capital, rooting in industry and building in-depth research capabilities are also an inevitable choice for analysts under the guidance of seller research and competition. The Brokerage Research Institute emphasizes industrial research, and the deep logic behind it is not difficult to understand.

First of all, for analysts, long-term roots in the industry can accumulate rich knowledge and have enough knowledge reserves to judge innovation trends, so as to put forward views that can stand the test of time and gain a long-term good reputation from investors. At the same time, analysts can help investors better grasp the industrial context and explore investment opportunities by continuously and closely tracking key listed companies and their related industrial chains.

The director of a research institute has said that the two core parts of capital markets are industry and capital, and the core role of seller research is to connect the two. "The essential element of all capital markets intermediary business is to have a deep understanding of the industry and listed companies and build trust with them. The research institute conducts focused, long-term and in-depth research on the industry, cuts into the industry and the company, and builds trust, which is also needed for other businesses."

Secondly, the overall market opportunities are gradually sinking. In the past few years, many investors have high hopes for core assets, and a group of well-known and highly competitive blue-chip stocks represented by large companies such as Kweichow Moutai, Gree Electric Appliances, and Ping An of China are in demand. In recent years, as public and private quantitative investment has gradually become a market hotspot, small and medium-sized companies have begun to gain popularity in the market. In recent years, the returns of small-cap indices are significantly higher than those of large-cap indices, and they are more flexible. Due to the low attention paid to small-cap stocks, there may be more pricing biases, thus creating more opportunities for quantitative institutions. And when the market’s attention moves down, sell-side analysts should also look down. Analysts with an industrial chain mindset can adapt to this situation faster and conduct in-depth research and exploration of valuable small and medium-sized companies.

Thirdly, with the penetration of new technologies such as AI and the Internet of Things into all walks of life, many high-quality enterprises have become cross-industry converters, and research on them also requires diverse knowledge. For example, the semiconductor industry chain is divided into design, manufacturing, packaging and testing, equipment and materials links, and product forms include computing, storage, sensing, power, simulation and radio frequency. Applications cover consumer, home appliance, industrial, automotive, medical and special industries. In the past, single industry research has no longer adapted to the development trend of the industry.

In order to adapt to this situation, the organizational structure of many research institutes has also been adjusted accordingly. An obvious trend is that more and more research institutes are beginning to open up the industry, extending the original scattered research groups in the form of industrial chains to form industry groups. In the 3.0 reform, the National Securities Research Institute is committed to opening up the internal industrial chain and encouraging joint coverage of industries.

"Taking the robot industry chain as an example, the entire robot industry may involve machinery, electronics, new materials and other aspects, and if you simply let the mechanical team study robots, there will inevitably be a relatively one-sided research perspective. After opening up the industry, analysts will have a stronger ability to observe the whole industry chain, which is empowering for the team."

Lu Ying said that with the increasing trend of industrial integration, Haitong Research has added meso research on the basis of past macro-micro research. On the one hand, it aggregates the industry from the perspective of industry and focuses on seven industrial chains. Among them, consumption, medicine, high-end manufacturing, new energy, and technology have become the focus of industrial research. On the other hand, it has increased regional joint research in meso to meet the requirements and trends of serving the development of the real economy.

At the same time, at the micro level, the strengthening trend of industrial integration has also led to further refinement of industry research, with some emerging interdisciplinary fields beginning to emerge, and the sub-industries under the original more than 30 industry levels further extended.

CITIC Jiantou Securities Research Institute has added artificial intelligence industry research to cope with the hot trend of AI development. In terms of industry, "we have specially set up an industry such as new energy vehicles and lithium batteries, which is derived from the intersection of the original electric and automotive research sectors." Wu Chao, director of CITIC Jiantou Securities Research Institute and head of the international business department, managing director, and chief analyst of the TMT industry, said, "For the expansion and contraction of the industry, in fact, you still need to smooth this cyclical cycle by enriching your customer types. In simple terms, it is to expand demand, not to adjust production capacity. In terms of research, it cannot be static. For some emerging industries, we choose to subdivide in the original 30 industries, because there will be many interdisciplinary disciplines."

In fact, the new trend of industrial development is driving changes in the demand, content, and methods of research, which prompts analysts to change the single company research perspective when doing research, and conduct cross-upstream, cross-disciplinary, and multi-angle comparative research to achieve research integrity.

Zhao Xiaoguang, vice-president of Tianfeng Securities and director of the research institute, told New Wealth that in-depth research is a system that needs to be built from the structure and invested systematically. Zhao Xiaoguang believes that the past research is a kind of non-systematic research. In the future, it should stand in the perspective of the entire industrial chain, analyze the trend evolution of the industry from a global perspective, and then analyze the impact of this change on the industry and related companies. "This kind of systematic research should be based on the integration ability of the industry itself, top expert think tanks and in-depth research capabilities."

At present, the Tianfeng Securities Research Institute is building the Brokerage Research Institute 2.0 system with the four-in-one research methodology of "policy + expert circle + research questionnaire + data technology", creating a new in-depth research paradigm.

Zhao Xiaoguang introduced that the goal of the "four in one" is to systematize and logically track policies, analyze the variables that affect policy factors, and then integrate policy research into macro, meso, industrial and corporate values to judge; the second is to upgrade the expert system, from the perspective of industry, conduct systematic interviews and surveys of high-end expert databases, form a judgment on the industrial logic of industrial trends, and turn expert services into data and products; the third is to change reverse research into positive research, tracking the upstream and downstream of an industry chain without dead ends, and generating positive research results from point to point.

In his opinion, the value of Tianfeng’s construction of an in-depth research system has been gradually confirmed. In the second half of 2022, the overall shock of class A shares, but the performance of the Xinchuang (information technology application innovation) industry chain is relatively good, and the Xinchuang sector is recommended by Tianfeng Securities from the industry to the strategy earlier at the relative bottom. This is the successful practice of the "four-in-one" research system. "At present, the in-depth research system around key industries has been basically completed. Next, it is very important to build models, replicate in-depth research to more industries, and establish a tracking system from the total amount to the industry to the enterprise to help customers better establish an investment system."

In the process of industrial research, the talent structure of the brokerage research institute has also gradually changed. From the new wealth survey, under the premise of maintaining the same high academic background, many leaders of the brokerage research institute have shown a preference for talents with industrial background, while in campus recruitment, talents with "science and engineering + finance" composite background are more favored.

Talent remains the key to determining the securities research competition landscape, "Dong Guangyang, a member of Huachuang Securities’ executive committee, vice-president and director of the research institute, told New Wealth." This is an asset-light industry with people as the core factor of production. Cultivating excellent talents, allowing them to maintain their enthusiasm for research, and then creating more value is the most critical. "

It is worth mentioning that by deepening the industry and building an in-depth research system, the overall ecology of the securities research industry may be changed to some extent.

For a long time, due to the high-intensity work, sell-side research has been considered by many to be a "youth food" industry, and analysts have been under pressure to "become famous as soon as possible". Today, deep cultivation of the industry requires analysts to track the development of the industry for a long time. Only with long-term persistence can it be possible to make research with a deeper understanding of the industry, which will also help analysts get rid of the age limit and prolong the career development cycle.

Nonetheless, in the short term, the competition for seller research will still be more intense. At present, the demand for recruitment in the industry has changed. Many directors of research institutes told New Fortune that the number of personnel is now close to the ideal state. Compared with increasing manpower, adjusting the talent structure will become its next focus. For institutes that are not very strong in seller research business, the need for downsizing is relatively stronger.

"According to the principle of factor sparsity, when the overall competition in the industry is more intense, there will be an era of capacity reduction. But in this process, the quality and value of the overall seller research will also improve, because in the competition, good analysts will be screened out, and in this process, the overall quality of the seller research will be improved."

05, Digital construction empowers in-depth research

In the competition, strengthening digital construction and building a platform to empower analysts are becoming a breakthrough point for large brokerages to research and break through.

Through digital technology investment, we can improve analysts’ information acquisition and processing efficiency, achieve data diversification and refinement, and help analysts make more accurate and in-depth judgments. By generating differentiated in-depth research reports, we have become one of the development directions of the platform strategy of large brokerages.

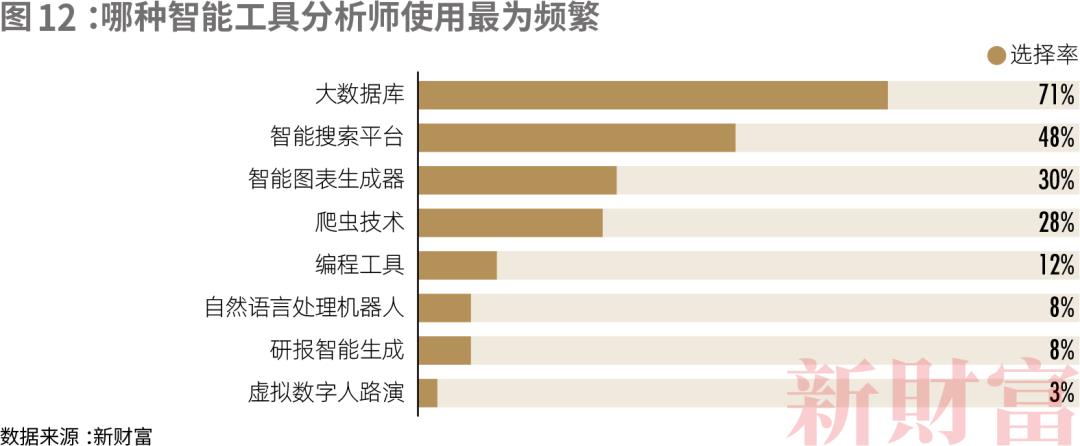

In fact, with the onset of the fintech wave, new technologies, including AI, have shown considerable speed of implementation, providing assistance to analysts in terms of broadening data collection, enriching information sources, and improving research efficiency. Among them, smart tools such as big data, intelligent search, intelligent chart generation, and crawlers have been frequently used by analysts in research work (Figure 12).

From the practice of international investment banks, digital construction is indispensable. The Boston Consulting Group (BCG) believes that digital breakthroughs will become a powerful weapon for brokerages to widen the gap and form their own brand characteristics.

Innovative technologies can also help research institutions to solidify their research data, research logic, and research models, thus precipitating the seller’s research capabilities and assisting research institutions in digitization and platformization. Some leading securities research institutes in China have data, analytical frameworks, theories, and research logic that have been accumulated for many years, and intelligent processing of data through financial technology can bring a certain platform effect to the research institute.

For example, the Tianfeng Securities Research Institute has built a data tracking research platform – Tianfeng Data Research Institute – by combining points, lines and surfaces. It precipitates industrial data and expert data, provides research and consulting services for the industrial and capital sides, and explores investment opportunities. Zhao Xiaoguang said: "The research system of the’four-in-one ‘is mainly based on two points. The first is based on experts, and the second is based on data. Around these two points, rooted in in-depth research, and at the same time, with lines as the core, that is, forming a closed loop of the upstream and downstream of the industrial chain."

At the same time, the use of digital technology to precipitate research data, models and methodologies, and the personal experience of senior analysts into platform capabilities and values, can enable the Institute to better realize the replication and inheritance of knowledge, allowing newcomers to grow faster, improve efficiency, and save training costs.

Taking Changjiang Securities Research Institute as an example, relying on its long-term accumulation, its research map system built by financial technology means can automatically capture, sort out and organize the data used by analysts, track and anticipate the industry’s prosperity, demand and supply in real time, and make auxiliary decisions for investment. Moreover, on the basis of the research map, it uses artificial intelligence technology to realize the construction of an investment system with fundamentals as the core, empowering researchers to better serve buyers and promote the transformation of sellers’ capabilities and the exploration of new business models.

Liu Yuanrui, president of Changjiang Securities, said in an interview with New Fortune that it is necessary to create a systematic platform that allows analysts to release more energy and create greater value.

On the individual level, in the face of the question of "whether artificial intelligence will replace analysts", more than 60% of analysts believe that this day has not yet come, and artificial intelligence has a mostly positive impact on their work, which can reduce work pressure and improve work efficiency.

06. Differentiated breakout of the research institute of small and medium-sized securities firms

Compared with large brokerages, the road to transformation for small and medium-sized brokerage research institutes is obviously longer.

First of all, it needs to gain a firm foothold in the competition with large brokerages for the sub-warehouse commission cake; secondly, on this basis, it needs to expand the service radius, expand the brand influence, and drive the development of other business of brokerages; in addition, in the internal coordination, it also needs to further explore and find a stable value realization model.

And this also determines the logic and play differences of the transformation path of small and medium-sized securities firms.

"The reduction of fees and commissions for public offerings has caused certain pressure on the seller’s business of brokers. Large brokers usually have more resources and advantages, and can provide more value-added services to make up for the reduction in profits caused by the reduction of fees and commissions for public offerings. Small brokers face more severe challenges due to their limited resources, resulting in relatively weak competitiveness." Zhu Keli, executive director of the China Information Association and founding director of the National Research Institute for New Economics, stressed that the seller’s business has reached a window period when it has to be reformed.

However, although large brokerages have certain advantages in terms of pricing and sales capabilities, it is difficult to achieve all aspects. For small and medium-sized brokerages, building a differentiated route and forming local advantages in some fields is still the key to competing with large brokerages. This requires small and medium-sized brokerages to make arrangements in advance, focus on specific fields and specific regions, and invest resources and manpower to form dislocation competition. For example, the Soochow Securities Research Institute focuses on local economic development, giving play to the advantages of rooting in and serving local areas.

In terms of undertaking industrial research clients, business consulting business, etc., some securities firms with special shareholder backgrounds have obvious innate advantages. For example, Cinda Securities Research Institute has formed a good synergistic relationship with shareholder China Cinda in project delivery.

China Cinda is one of the four major state-owned AMCs (Asset Management Companies) in China. Its main businesses include non-performing asset management and financial services. Among them, non-performing asset management is the core business, and its revenue accounts for 78.9% and 70.5% of its total revenue in 2021 and 2022, respectively. In 2022, the total assets of its non-performing asset management segment were 991.888 billion yuan, and the total revenue was 57.089 billion yuan. Whether it is non-performing asset disposal or foreign investment, many of them need to rely on research institute support.

Cheng Yuan, director of Cinda Securities Research Institute, told New Wealth that the collaborative group business is an important positioning of Cinda Securities Research Institute. "China Cinda is a financial central enterprise mainly engaged in non-performing asset processing and alternative investment, with total assets exceeding 1.60 trillion yuan and annual investment of nearly 300 billion yuan. Many projects require the joint participation of the research institute, including but not limited to providing research opinions on project investment for industry research and enterprise research. Therefore, the group has long attached great importance to the research institute. For the research institute, the group is our important strategic customer."

On the other hand, the development experience of overseas boutique investment banks has also become one of their magic weapons by leveraging their unique businesses to break through.

In the 1970s, the Nasdaq national trading system began to operate, and the demand for investment banking business from small and medium-sized enterprises showed a explosive growth. At the same time, the merger and acquisition policy was loose, and the wave of mergers and acquisitions of small and medium-sized enterprises by large enterprises in the United States was on the rise. Goldman Sachs established the first merger and acquisition department on Wall Street, providing consulting services for small and medium-sized enterprises to resist hostile takeovers, avoiding direct competition with other investment banks in large corporate clients, and gradually became one of the top investment banks.

Some investment banks choose to deeply cultivate a certain customer group or region. Boutique investment banks represented by Evercore, Moelis and Lazard make subtractions in their business and choose to focus on individual businesses, such as investment and financing, listing, restructuring, mergers and acquisitions, corporate governance, and financial management. One or several core consulting services, so as to achieve a breakthrough.

Under the pressure of public fundraising and fee reduction, some research institutes need to make trade-offs on large and comprehensive research operations and move towards high-quality research that combines their own resource endowments.

Although in the short term, seller research may have a more intense competitive ecosystem, in the long run, valuable research will still stand out despite the survival of the fittest.

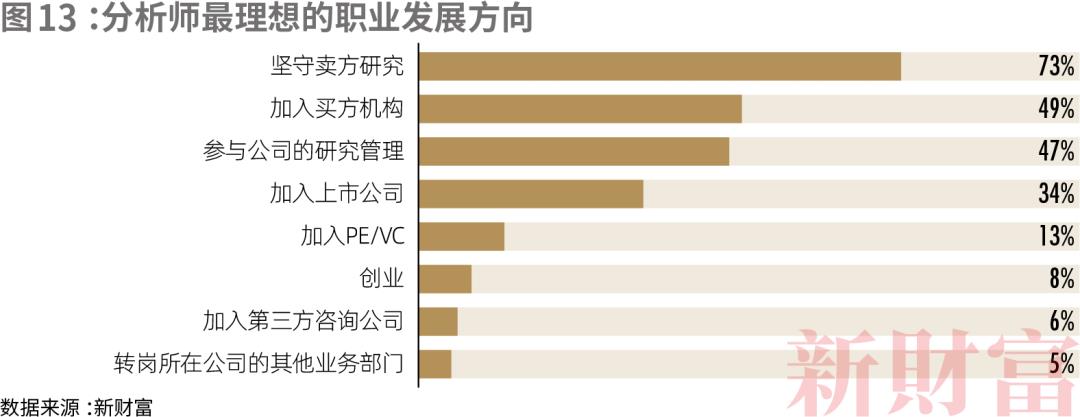

When it comes to career prospects, while 60% of analysts believe that increased competition requires more effort to maintain their current industry position, more than 70% still believe that sticking to sell-side research is the most ideal career development direction (Figure 13).

Adhering to the original intention, promoting research to return to the source, and better serving the capital markets and the real economy will continue to be the key to the high-quality development of the securities research industry in the new situation.